Offshore Fund Services: From Cost Arbitrage to Capability Arbitrage

May 11, 2026

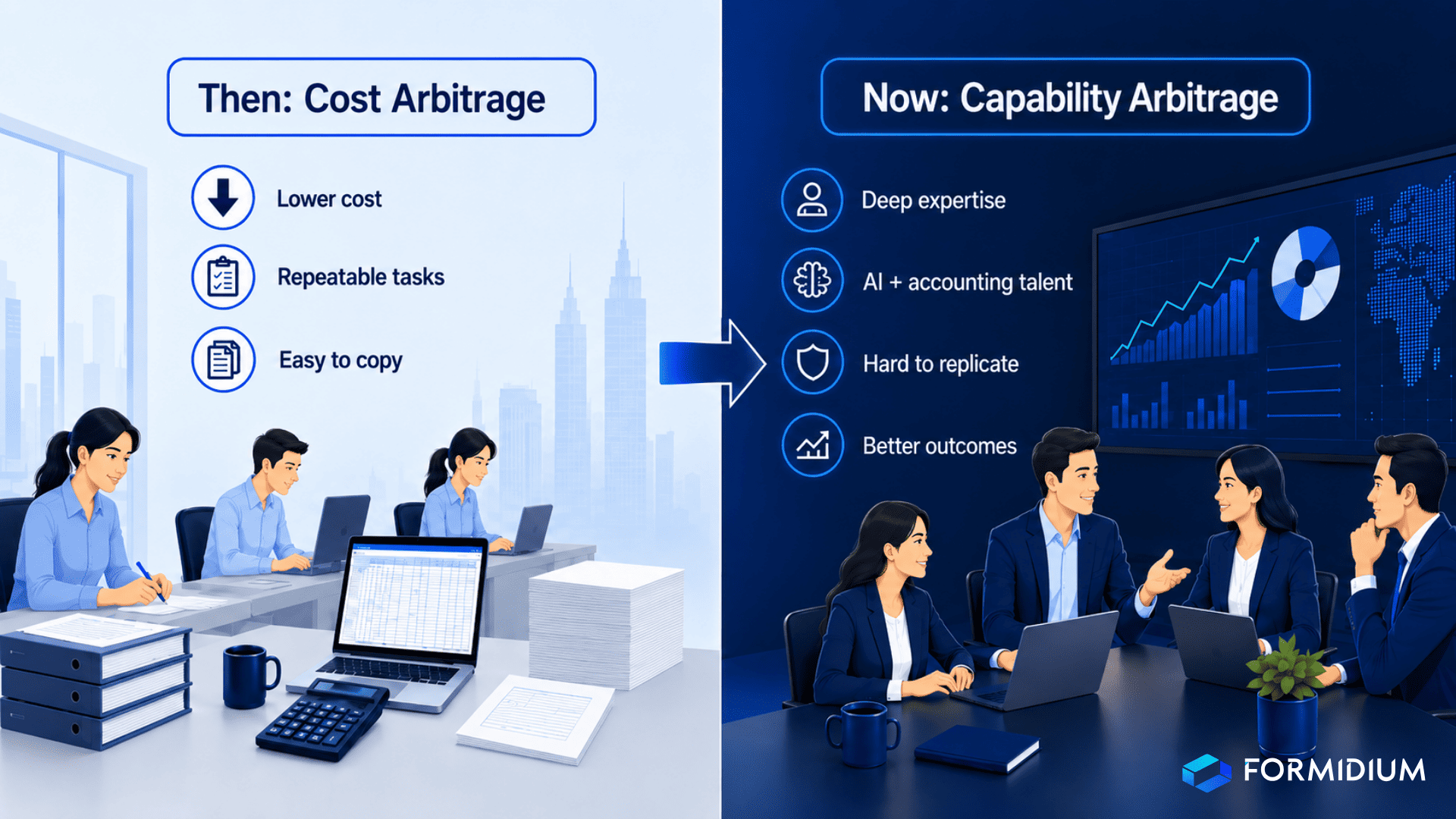

For the better part of three decades, offshoring in fund administration was sold as a cost story. Cheaper labor, lower overhead, slimmer invoices. That pitch worked because it was true at the time, and the industry built itself around it.

That story is over. Every administrator now has offshore teams. Every administrator now claims the same cost structure. The arbitrage that defined a generation of fund services has commoditized.

But something else was happening underneath the cost story, quietly, for thirty years. The same workforce that was originally hired to do cheap, repetitive accounting work was learning. Compounding. Specializing. Moving from junior qualified accountants reconciling cash to senior partners running global delivery for trillion-dollar platforms.

The offshore advantage didn't die. It evolved. Cost arbitrage gave way to capability arbitrage, and the firms that understand the difference will define the next decade of fund administration.

The Compounding That Nobody Was Watching

When offshoring began in fund services in the early 1990s, the work was simple by design. Bank reconciliations. Trade confirmations. Basic NAV checks. The thesis was obvious: take repeatable tasks, ship them to a lower-cost market, save money.

What happened next is the part most managers missed.

The accountants who started doing those reconciliations didn't stay junior forever. They moved into supervisory roles. They trained the next cohort. They handled increasingly complex fund structures. Hedge funds. Then private equity. Then real estate. Then crypto. Each cycle pulled the same workforce up the value chain.

Today, the senior partners running offshore delivery for the largest global administrators are the same people who were doing entry-level accounting work in 1995. They have seen every market cycle, every regulatory shift, every product innovation in alternative investments. That isn't outsourced labor. That is institutional memory, built over a generation, in a workforce that the industry still talks about as if it were 1998.

The talent stack has thickened across every level. The junior qualified accountants entering the workforce today are joining teams that already contain three decades of accumulated expertise above them. The training is faster. The standards are higher. The output quality compounds.

This is not a cost story. This is a capability story. And it took thirty years to build.

Where the Capability Actually Lives

Not all offshore hubs are equal. Three jurisdictions matter most for fund administration today, in this order.

India

India is the deepest pool, and it isn't close. The country produces more chartered accountants annually than most other jurisdictions combined. The fund services industry has been operating there at scale since the mid-1990s, which means it now has senior leaders with three decades of direct experience in alternative investment accounting.

But here is what makes India structurally different from every other offshore hub: it is also the world's deepest pool of technology talent. The same labor market that produces fund accountants also produces software engineers, data scientists, and AI specialists. They sit in the same cities, often in the same companies, sometimes on the same floor.

This matters now because fund administration is becoming a technology problem as much as an accounting problem. AI agents, agent-to-agent communication, intelligent data ingestion, automated reconciliation. The administrators who will lead the next decade are the ones who can fuse deep accounting expertise with deep technical capability. India is the only jurisdiction where both pools exist at scale, in the same workforce, with the cultural and operational continuity to combine them.

That is not a cost advantage. That is a capability moat that took thirty years to build and cannot be replicated quickly anywhere else.

Philippines

The Philippines built its position more recently than India, but it built it well. Strong English fluency, a service culture oriented around financial operations, and a workforce that has matured significantly over the past fifteen years. The depth in fund accounting is real, particularly in middle-office functions and investor servicing.

Where India brings a fusion of accounting and technology talent, the Philippines brings disciplined operational execution. The two are complementary, and the firms that use them well treat them that way.

Poland

Poland has emerged as the European counterpart to the Asian hubs. The talent is technically strong, multilingual, and operates within EU regulatory frameworks, which matters for European fund managers and for firms that need timezone coverage closer to London and Luxembourg.

Poland is smaller than India or the Philippines in raw scale, but the quality is consistent and the integration with European markets is seamless. For administrators serving cross-border European structures, it is increasingly indispensable.

Why Capability Arbitrage Beats Cost Arbitrage

The shift from cost to capability changes the math in ways most managers haven't fully internalized.

Cost arbitrage was zero-sum. You either paid less for the same work, or you didn't. The advantage was easy to copy and easy to compete away. That is exactly what happened. Every administrator now has offshore teams, every administrator now has roughly comparable cost structures, and the cost story has lost most of its meaning as a differentiator.

Capability arbitrage is different. Capability compounds. A team with thirty years of accumulated expertise in real estate fund accounting cannot be matched by a team standing up the same function from scratch, no matter how much money you throw at it. The depth has to be earned over time, and time is the one input you cannot accelerate.

This is why the strongest offshore operations are no longer just cheaper. They are better. Better at handling complex fund structures. Better at navigating ambiguous transactions. Better at supervising the AI systems that are starting to handle the repetitive work. The senior accountants who once would have been training someone to do a manual reconciliation are now training agents to do it instead, and validating the output with a level of judgment that took decades to develop.

And here is the part the industry doesn't say out loud often enough: you still get the cost advantage. The labor economics haven't reversed. India, the Philippines, and Poland still cost meaningfully less than equivalent talent in New York, London, or Singapore. The difference now is that you are no longer paying less for the same thing. You are paying less for something better.

That is capability arbitrage. Both sides of the trade work in your favor.

The AI Multiplier

AI is amplifying the capability gap between offshore operations that have invested in their workforce and those that haven't.

In the cost-arbitrage era, the offshore model worked because labor was cheap enough to absorb manual processes at scale. You hired more people to do more work. The unit economics held up because each incremental accountant was inexpensive.

AI breaks that model in both directions. For administrators that built their offshore footprint as a labor arbitrage play, AI is an existential threat. The cost advantage of cheap manual labor disappears the moment automation can do the same work for less. If your offshore strategy was built around volume and headcount, the floor is moving.

But for administrators that built their offshore footprint as a capability play, AI is a multiplier. The senior expertise that took decades to develop is exactly the input AI needs to function well. Agents have to be configured, supervised, validated, and corrected. That work demands judgment, not throughput. The accountants who can do it are the ones who already understand the underlying logic deeply enough to spot when an agent is wrong.

This is where India's dual talent pool becomes a genuine moat. The fund accountants who have spent a generation building expertise in alternative investment operations are sitting next to the engineers building the AI systems that are starting to automate that work. The feedback loop between domain expertise and technical implementation is faster, tighter, and more iterative than in any other market. That loop is where the next generation of fund administration infrastructure is being built.

The administrators that understand this aren't moving offshore work back onshore. They are moving more of the high-value work offshore, because that is where the capability density is highest.

What This Means for Fund Managers

If you are a fund manager evaluating administrators, the offshore conversation needs to change.

Stop calculating how much your administrator's offshore team costs. That answer is roughly the same across the industry now. Start asking what the offshore team can actually do.

The right questions are different in this environment. How long has the senior leadership in your offshore offices been doing fund accounting? Are the people supervising your fund's books five-year hires or twenty year veterans? Does your administrator have an AI game plan starting with a capable tech team? Can they show you anything tangible that the team has produced? Is there a pipeline between your accounting team and the engineers building your administrator's technology, or are they siloed?

The administrators that win the next decade will be the ones whose offshore operations have moved from labor pools to capability centers. The two look similar from the outside, but they are fundamentally different businesses. One competes on price. The other compounds expertise.

You can usually tell which is which within ten minutes of a real conversation with the operating team.

The Story Most Administrators Are Still Telling

Here is the uncomfortable part. Most administrators are still selling offshore the way it was sold in 2005. Cheaper labor, lower cost, more efficient processing. That pitch is dated, and it gives away how the firm actually thinks about its workforce.

If your administrator is still describing its offshore presence primarily in cost terms, that tells you something important. It tells you they treat that workforce as a line item, not an asset. It tells you they probably haven't invested in the senior expertise that makes offshore operations valuable in the AI era. And it tells you that when the cost-arbitrage floor finally collapses, which it is doing now, they don't have a capability story to fall back on.

The administrators that have been quietly investing in capability for the past two decades aren't talking about cost much anymore. They are talking about expertise, technology integration, and the judgment that AI systems still cannot replicate. That shift in language reflects a shift in substance. It is worth listening for.

Final Thought

Offshoring in fund services started as a cost play, and for a long time that was enough. It isn't anymore.

What thirty years of compounding actually built was something more durable than cheap labor. It built deep, layered expertise in alternative investment operations, concentrated in jurisdictions that also happen to be where the world's technology talent lives. That is the foundation the next generation of fund administration is being built on, and it is the reason the offshore model is more relevant today than it was when it was just about saving money.

Cost arbitrage is over. Capability arbitrage is just getting started. And the fund managers who recognize the difference will end up with administrators that are not just cheaper, but materially better at the work.

About the Author

Shalin Madan is co-founder of Formidium and former hedge fund manager with 25 years in alternative investments and fund administration. At Formidium, proprietary technology supports over $34 billion in AUA, delivering institutional-grade capabilities with boutique-level service for real estate, private equity, venture capital, hedge funds and digital asset funds.