The Nokia Moment in Fund Administration: Why Europe Is Losing, Why U.S. Tech-First Firms Are Winning, And Why the Window Is Closing Fast

May 13, 2026

In 2007, Nokia owned the mobile phone market. Iconic brand. Global distribution. Engineering talent that the rest of the industry envied.

Then Apple shipped the iPhone.

Nokia did not lose because they could not build a touchscreen. They had the engineering. They had the patents. They lost because they thought the iPhone was a better phone, when it was actually a new operating system for a new economy. By the time the leadership team understood what had happened, the structural advantage was gone.

You cannot catch up to a platform shift after the platform has already shifted.

I think about this every time I sit across from a fund manager who is still working with a European fund administrator that has not meaningfully changed in fifteen years. Because what is happening in fund administration right now is exactly the same shift, in slow motion. Europe is Nokia. The U.S. tech-first firms are the iPhone. And the window to act on that is shorter than most managers realise.

Why Europe Is Losing: The Prestige Trap

To understand why European fund administration is structurally vulnerable, you have to understand what it was actually built on.

It was not built on technology. It was built on jurisdiction.

For thirty years, the entire value proposition of European fund administration was geographic credibility. Luxembourg meant institutional. Dublin meant respectable. The Channel Islands meant tax-aware sophistication. Zurich meant private wealth pedigree. Putting one of those names on your service provider list signalled to LPs that you had cleared a quality bar, even if no one could really explain what the bar was.

That signal worked because the underlying work, fund accounting, was genuinely complex and genuinely opaque. LPs could not easily verify what was happening inside the books, so they relied on jurisdictional reputation as a proxy. The administrators got rich on the proxy.

And then they built their entire operating model around protecting it.

Headcount as a moat

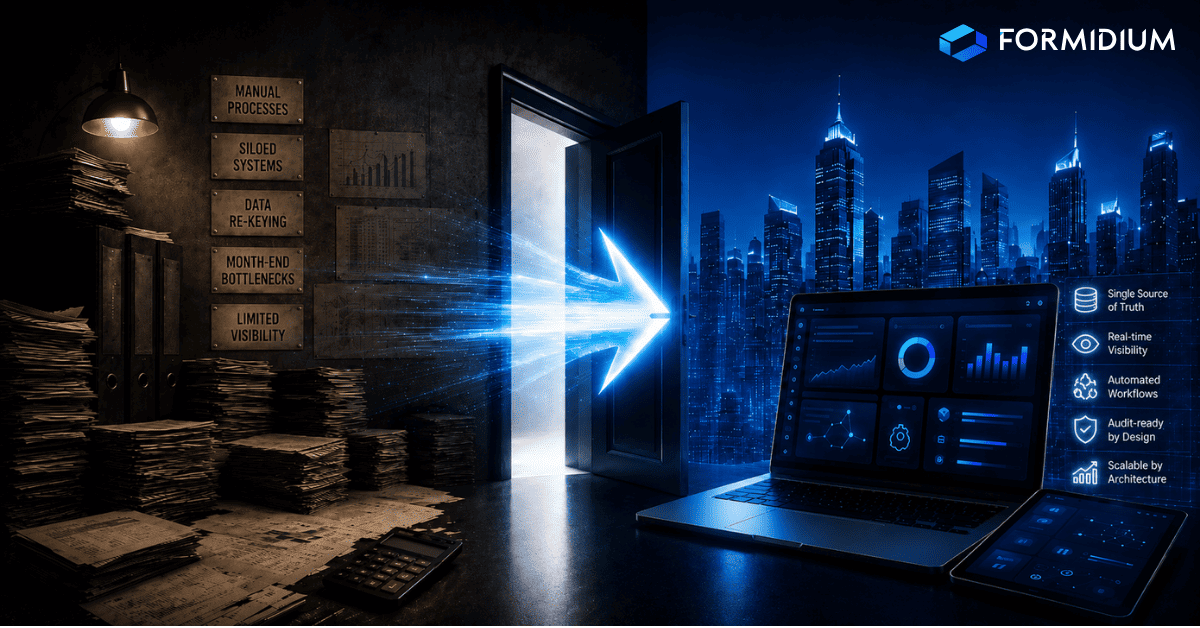

Walk into the back office of a major European administrator and you are not looking at a technology company. You are looking at a labour company with a brand on the door.

Hundreds of accountants in Luxembourg or Dublin, marked up to LP-facing rates. Thousands more in offshore centres in India, the Philippines, Mauritius, doing the actual data entry and reconciliation work that gets re-stamped under the European banner. Manual journal construction. Spreadsheet-based reconciliation. Investor data being re-keyed from onboarding documents into accounting systems that the firm does not even own.

The technology layer, when it exists, is mostly cosmetic. A polished portal here, a reporting dashboard there, both sitting on top of the same manual plumbing that has run the books for two decades. None of it touches the ledger. None of it changes the cost structure.

This worked when capital was flowing and LPs accepted whatever fees came with the brand. It does not work now. Offshore wages in India have climbed 50 to 100 percent in the last few years as staff get poached between firms. Brand-heavy administrators carry enormous fixed costs to cover. Firms that grew through acquisition are servicing the debt from those deals on the back of client invoices. Fees are going up across the board, and the explanations getting handed to managers are getting thinner.

That is not a story about temporary cost pressure. That is a story about a model that scales the wrong way.

Renting the engine

Here is the part most managers never see. A large portion of European administrators do not own the accounting platform that runs their clients' books. They license it from a third party.

That single fact constrains everything. When you do not own the system of record, you cannot embed automation into the journal logic. You cannot redesign the reconciliation workflow. You cannot govern the audit trail. You can buy a portal that wraps around the rented engine, but the engine itself is not yours to change.

This is why so much of the AI announcement traffic from incumbent administrators reads as theatre. A chat interface bolted onto a static portal. A summary tool sitting on top of manually maintained books. None of it moves the cost structure, because none of it touches the actual ledger.

Real automation requires owning the engine. The European model was not built that way, and you cannot retrofit it now without rebuilding the firm.

Why this is the Nokia position

Nokia did not look fragile in 2007. Market share was strong. Margins were healthy. The brand was iconic. The fragility was structural and invisible from the outside.

Same thing here. The European incumbents look dominant because the AUA numbers are big and the logos are famous. The fragility is in the architecture. They are running a labour-driven model in a market where the economics are about to favour automated models. They are protecting brand value in a market where LPs are starting to ask harder questions than the brand can answer.

Dominant on paper. Structurally vulnerable underneath. Convinced the brand will carry them through whatever is coming next.

That is the Nokia position, exactly.

Why U.S. Tech-First Firms Are Winning

The U.S. tech-first fund administrators are not just better-resourced versions of the European model. They are a different species of firm, built around a different set of beliefs.

They believe technology belongs inside the accounting and controls layer, not around it. They believe the firm should own the system of record, not rent it. They believe automation should be embedded into the ledger, not bolted onto a portal. They believe accountants should supervise systems, not feed them. And they believe transparency should be operational, meaning clients can see the books for themselves, not just the PDFs that get sent to them at month-end.

Those beliefs sound abstract until you see what they produce.

Owned architecture, end to end

In a U.S. tech-first firm, onboarding, accounting, reconciliation, reporting, and compliance all sit on a single data layer. Investor data captured during onboarding flows directly into the general ledger without anyone re-keying it. Capital call data triggers the related allocations and capital account updates automatically. Reconciliation runs continuously rather than as a month-end fire drill.

This is not a feature. It is the operating model. And it is only possible when the firm owns the architecture, because integration that deep cannot be assembled out of third-party components.

The downstream effect on the cost structure is significant. Every hand-off in a fragmented system is a place where errors get introduced and people are required to fix them. Eliminate the hand-offs and you eliminate the headcount that exists to manage them.

AI agents inside the ledger

This is where the gap between iPhone and Nokia becomes structural rather than cosmetic.

In a tech-first architecture, AI agents are not a chat interface. They are autonomous systems running inside the accounting engine. They classify journal entries against embedded rules, run allocation waterfalls, perform NAV reconciliation across custodial feeds, calculate management fees and performance allocations, surface only true exceptions for human review, and maintain a complete time-stamped audit trail as they go.

The accountant's role shifts from constructing entries to supervising the systems that construct them. That is not a marginal efficiency gain. It changes how a fund administration firm scales. The marginal cost of taking on the next fund is no longer headcount. It is configuration.

In a Nokia-style labour model, every new fund requires more accountants. In an iPhone-style architecture, every new fund runs through the same automated logic, the same agent-driven reconciliation, the same single source of truth. Marginal cost actually declines as scale grows.

Two firms can both call themselves fund administrators. The economics of the businesses are not the same.

Agent-to-agent communication is killing switching friction

There is a reason European incumbents have been able to retain clients for years past the point where the service stopped being competitive. Switching was painful. Data lived in proprietary formats. Allocation logic and exception handling lived in the heads of senior accountants. Audit history was hard to extract. Transitions required months of senior people on both sides manually reconstructing how the books had been maintained.

That friction was not an accident. It was the moat.

AI agents are draining that moat. When the outgoing administrator's agent can transfer structured data, allocation logic, and audit history directly to the incoming administrator's agent, with automated validation at every step, the manual reconstruction phase compresses from months to days. Parallel operations that used to last two quarters now run for weeks. The audit trail travels intact. The cutover becomes a project rather than an ordeal.

Once switching cost collapses, the only thing keeping a manager with a bad administrator is inertia. And inertia is not a long-term retention strategy.

Why the Window Is Closing Fast

Three things are accelerating right now, and they are accelerating together. Each one would be significant on its own. Together they are why the gap between Europe and U.S. tech-first firms is no longer a gap that can be closed.

Operational economics are diverging, not converging

Every quarter that an integrated, AI-native platform runs, the cost gap widens. Cost per fund goes down for the tech-first firm and up for the brand-heavy incumbent. That is not a small swing. Roughly 25 to 40 percent of the operating cost base in fund administration is directly addressable through automation embedded in the system of record. That is structural deflation for the firms that have it, and structural inflation for the firms that do not.

You cannot price your way out of that gap. You can only architect your way out, and architecture takes years to build properly. By the time a Nokia-style administrator commits to the rebuild, the iPhone-style firms are five generations of platform development ahead.

LPs are putting these questions into diligence

This is the part that should worry the European incumbents the most, and it is the part that gets discussed the least.

Five years ago, putting a Luxembourg or Dublin administrator on the service provider list checked the institutional credibility box and ended the conversation. That is no longer how sophisticated LPs operate. The questions showing up in operational due diligence questionnaires now are operational, not jurisdictional.

Does the manager have direct access to the general ledger? Is there a complete, time-stamped audit trail for every journal entry, allocation, and adjustment? Can the manager drill down from NAV to the underlying investments and the underlying allocations in real time? Are investor allocations visible live, or do they wait for month-end? Is onboarding actually integrated with the books, or is it a DocuSign portal masquerading as digital infrastructure? How quickly can the administrator produce a clean data export, and in what format? What happens to the audit trail if the manager ever needs to switch?

These are not curiosity questions. These are diligence questions. The LP community is starting to understand that operational risk lives in the architecture of the administrator, not in the brand on the cover sheet, and the questions they ask are evolving accordingly. Allocators with U.S. pension capital behind them are already running this playbook. The rest of the LP base will follow, because once the more sophisticated allocators have framed the questions, the questions become the standard.

Brand-driven administrators struggle to answer those questions because the answers depend on architecture they do not own. A polished portal cannot fake a real audit trail. A reporting dashboard cannot manufacture drill-down access if the underlying data is not structured for it. A glossy onboarding interface cannot hide the fact that investor data is being re-keyed manually behind it. The questions LPs are now asking are the exact questions that brand-heavy infrastructure cannot answer well.

What used to be a credibility check has become a capability check. Jurisdiction does not survive that shift. Managers whose administrators cannot answer cleanly are going to find that conversation getting harder every diligence cycle.

The first wave of switches has started

For years, the case for switching was rational on paper but irrational in practice, because the disruption seemed too costly to absorb. That calculation has flipped.

When the first wave of managers moves to U.S. tech-first administrators and the move actually goes smoothly, when parallel operations close in weeks instead of quarters, when the data migrates cleanly through agent-driven transfer, when the audit trail survives intact, the disruption story that European incumbents have been telling for years stops being persuasive. The next ten managers see what happened and start their own evaluations. Then the next fifty.

Platform shifts do not move in trickles. They move in waves, because the social proof of clean transitions compounds faster than the incumbents can rebuild credibility. Nokia did not lose customers gradually. They lost them in a rush, once the iPhone proved itself. Fund administration will look the same.

The Risk Most GPs Are Not Pricing In

Cost and capability are usually framed as a present-day issue. They are actually a forward-looking issue, and that is the part most GPs are not thinking about hard enough.

The strategy you launch next is not the strategy you have today

The asset classes attracting capital five years from now are not going to look like the asset classes that defined the last cycle. Private credit is fragmenting into sub-strategies that did not exist as standalone products a decade ago. Tokenized real-world assets are moving from concept to fundable mandates. Digital asset funds are institutionalising. Hybrid structures that blend private equity, venture, and real assets are getting written into LPAs that did not contemplate them five years ago. Continuation vehicles, secondaries, semi-liquid evergreen structures, retail-accessible private market vehicles, all of these are growing faster than the operational infrastructure most administrators were built to support.

Every one of those structures asks something different of the accounting engine. Different fee mechanics. Different waterfall logic. Different investor reporting cadences. Different reconciliation requirements. Different regulatory contexts.

In a labour-driven administration model, every new structure means a new manual playbook, a new training cycle for the offshore team, a new layer of spreadsheets glued to the rented accounting platform. The lead time to support a new strategy is months, sometimes longer. And the cost to do it gets passed straight to the manager, because the only way the administrator can stand it up is by adding people.

In a tech-first architecture, supporting a new strategy is a configuration problem. The ledger logic, the allocation engine, the agent-driven reconciliation, all of it can be reconfigured for new mechanics without rebuilding the operating model. The lead time is weeks, not quarters. The marginal cost is small, not large.

That gap matters enormously when you are a GP trying to be first to market with a new strategy. The administrator that cannot move at the speed of the market is not just expensive. They are a constraint on the funds you can launch.

Costs do not stay where they are

There is a quiet assumption in a lot of GP-administrator relationships that current pricing is roughly the steady state, and the only direction it goes is mild inflation. That assumption is not safe.

In a labour-driven model, costs scale with complexity and headcount. As regulatory requirements grow, as reporting cadences accelerate, as new asset classes demand new operational handling, the only response a labour-driven administrator has is to add people. Those people get more expensive every year. The complexity does not slow down. The fees keep climbing.

Worse, the price increases are not really being driven by anything the GP is getting back. They are being driven by the administrator's own cost structure breaking under its own weight. Wage inflation in offshore centres. Acquisition debt. Retention bonuses to keep senior people from leaving. The GP pays for the administrator's structural problems, not for better service.

In a tech-first model, the curve runs the opposite direction. As automation deepens, as agents take on more of the workload, as the architecture absorbs new strategies through configuration rather than headcount, the marginal cost per fund actually declines. That is not theoretical. It is the entire point of building the firm around technology in the first place.

Five years from now, the gap between what a tech-first administrator costs and what a labour-driven administrator costs is going to be uncomfortable. Ten years from now it is going to be unjustifiable. The GPs locked into the labour-driven model will be paying meaningfully more for meaningfully less, in front of LPs who can see the gap clearly.

The LP question that is coming

Sophisticated LPs are already starting to ask whether a GP's administrator can support the strategies the fund will plausibly want to launch in the next five to seven years. That question used to be a curiosity. It is becoming a diligence item. LPs do not want to commit to a relationship where the operational infrastructure constrains the GP's ability to evolve the platform.

If the answer to that question depends on whether the administrator can hire fast enough, the answer is not strong. If the answer depends on whether the architecture can be configured to handle new mechanics, the answer is much stronger. LPs are starting to know the difference, and they are going to weight it accordingly.

A GP whose administrator cannot keep up with where the market is going is not just facing a cost problem. They are facing a fundraising problem they have not seen yet.

What This Means If You Are a Fund Manager

The harder question is not whether the shift is happening. It is what to do about it before the gap becomes uncatchable for the firm administering your books.

If your administrator cannot explain in plain language what they own versus what they rent, that is information. If their AI story is a chat box on top of a portal rather than agents inside the ledger, that is information. If asking for a clean data export feels like an audit, that is information. If you cannot drill down from your NAV into the underlying allocations without sending an email, that is information. If the relationship runs on personal trust with the accounting team rather than on system access you can verify yourself, that is information. If you cannot get a confident answer about how quickly they could support a new strategy you are considering, that is information.

None of these are individually disqualifying. Together they form a profile. They tell you whether you are working with a Nokia or with something built for what comes next.

The cost of switching is finite and front-loaded. The cost of staying with the wrong administrator compounds every quarter. In rising fees. In operational risk. In time you spend chasing answers that should already be visible. In LP questions you cannot answer cleanly because your administrator cannot answer them cleanly first. In strategies you cannot launch because your operational infrastructure cannot keep up.

Final Thought

Nokia did not lose to Apple because Apple had better hardware. Nokia lost because the entire definition of what a phone was had changed underneath them, and they kept selling the old definition until the market stopped buying it.

Fund administration is in the same place. The European incumbents are still selling jurisdiction, headcount, and brand. The U.S. tech-first firms are selling owned architecture, AI agents inside the accounting engine, operational transparency the manager can verify, and an economic model where marginal cost goes down as scale grows.

Both groups are calling themselves fund administrators. Only one of them is doing it in a way that will still make economic sense in five years, and only one of them can keep up with the asset classes that will define the next cycle.

The fund managers who recognise the shift early do not just end up with a better administrator. They stop subsidising a model that is quietly becoming obsolete at their expense, and they put themselves in front of the LP questions that are coming rather than behind them.

The window is open right now. It will not be open forever.

About the Author

Achim Denkel is Managing Director Sales & Marketing Europe at Formidium. He has more than 20 years of experience in fund services, fintech and alternative Investments, with senior leadership and board roles across Germany, Luxemburg and Liechtenstein. He focuses on driving Formidium's growth and supporting alternative asset managers with technology - driven solutions.